Chapter Seven

Sources of Profit and Loss

Recent records of the private enterprise system show that prosperity can only be maintained through a variety of policy changes that reflect a clear understanding of how the profits of private enterprise are created. This understanding will pin point the real sources of profit, and the real sources of loss in the nation's economy.

Recent records of the private enterprise system show that prosperity can only be maintained through a variety of policy changes that reflect a clear understanding of how the profits of private enterprise are created. This understanding will pin point the real sources of profit, and the real sources of loss in the nation's economy.

These real sources of loss should not be confused with the appropriate percentage of National Income that must be earned as a cost to the private enterprise system and expressed on the right side of the T-chart. This percentage should range from 65% to 67% of National Income regardless of the level of National Income. With this knowledge and the knowledge of how the profits of private enterprise are created and sustained, it is possible for law makers to move the economy toward more profitable areas of endeavor. National Income will then grow in accurate ratios and banks will store more debt free money (wealth) and fewer promissory notes (debt). Then government will function as a balance wheel rather than a rich uncle.

During periods of prosperity, the T-charts reflect a relationship of about 2 parts income derived from the cost of production to 1 part income derived from the profits of private enterprise, (before taxes), that together comprise National Income. This approximate ratio occurred for many years during the 20th century. The T-charts also show the ratio between these two sides of national income has changed dramatically during the last two decades. During this recent period, profits have severely decreased as a percentage of National Income and the ratio moved to 5 parts cost for every 1 part profit.

This decrease in profit has occurred simultaneously with several other changes. Two of these changes are the increased use of interest in the production economy, and the dramatic increase in supplements to wages. A third factor, not previously discussed, is the complete elimination of farm income as a component of proprietor's income and therefore as a contributor to the profits of private enterprise.

Some economists explain that during recent years America has become more "service oriented." Some of those extra services are health care, and the interest costs associated with pension plans. Additionally, the economy removed the "excess resources from agriculture."

Ironically, increased health care costs and the increased use of interest are seen as inevitable by most economists, while any increase to the farm portion of raw materials income is considered inflationary. This conclusion produces several questions:

1. Should the economy become more service oriented and less production dependent in the future?

2. If a service based economy is preferable to a production based economy, why are the profits of private enterprise deteriorating while the economy becomes more service oriented?

3. Is a service economy sustainable?

The full impact of America's "growing service economy," is discovered by separating the T-chart into two series of years. This analysis is displayed on Table 24 & 25.

Table 24, focuses on the ratios of income derived from the cost of production on the right side of the T-chart and the profits of private enterprise remaining on the left side of the T-chart for the years 1929 through 1980.

This confirms a long term ratio of 2 parts cost to 1 part profits (before taxes) for almost 40 years. However, during the 1970's, this profit ratio began a deterioration that was inversely proportional to the unprecedented expansion of public and private debt.

Table 25 confirms the deteriorating profit ratios of the modern "service economy." During the 13 year period (1981-93) costs have stabilized at a 5 to 1 ratio to profits, which illustrates a serious reduction in America's profitability. Some argue that a new permanent level of profitability has been established in the global arena, and America has adapted to this change. However, to understand the impact of 5 to 1 cost to income ratios (1981-93), please review the following records provided by the Department of Commerce.

AMERICA HAS BEEN SUBMERGED IN DEBT

Recent levels of low profitability have increased debt expansion. In previous chapters the government debt component of debt expansion was analyzed. However, government debt is only a part of the debt problem, because 2/3 of all debt is of private origin. Private debt is the business, investment, and consumer debt incurred by individuals and companies.

By analyzing available data on both public and private debt it is possible to determine the level of National Income necessary to service and repay America's entire debt obligations. This proves a lot more net income (left side of the T-chart income) is required if debt as a percentage of National Income is to ever be reduced and replaced with savings.

To stabilize the most recent cost to income ratios at 5 to 1 during the 1980's and 1990's, the total public and private debt was increased from approximately 4 Trillion Dollars to 14 Trillion Dollars. This was a three fold expansion of debt during a time when National Income only doubled from about 2.5 Trillion Dollars in 1981 to about 5.1 Trillion Dollars in 1993.

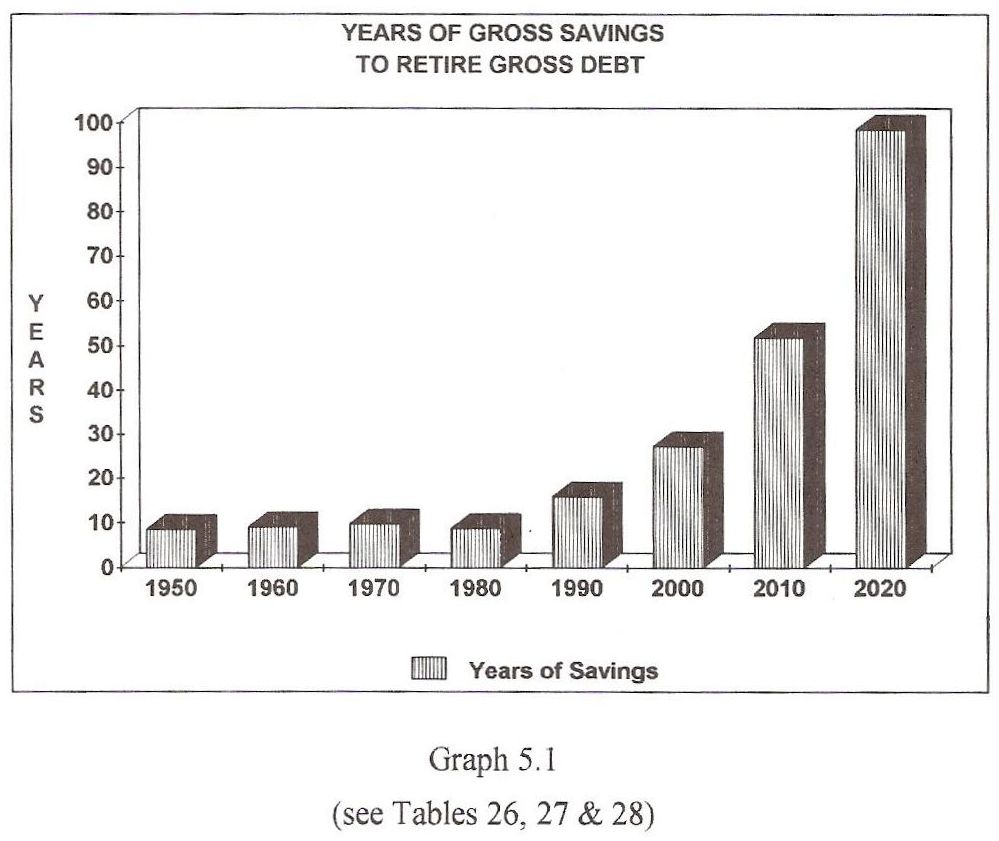

To place this debt in context, we calculated the amount of accumulated savings necessary to pay off accumulated debt using the annual net income generated by the economy. During the period of 1946 through 1980, America averaged approximately 9 years indebtedness as a society. The 1946 to 1980 statistics are reflected on Table 26.

Table 27 suggests the current debt situation has become non-sustainable

because America has borrowed more than 17 years of savings. In other words, in 1993, over 17 years of savings was required to repay total public and private debt. Today, debt is still growing faster than Gross Savings or National Income, and overall costs are growing in ratio to profits. In fact, current trends demand that every citizen who is 44 years of age or older must theoretically work until retirement to repay their pro-rata portion of our nation's cumulative debt without contributing anything to Domestic Wealth.

This situation is projected forward on Graph 5.1.

Table 28 uses recent trends to demonstrate that decreasing levels of profitability are de-coupling the historical ratios of Gross Savings to National Income. The table suggests that if current trends continue, by the year 2016, a lifetime of Gross Savings (76 years) will be required to repay accumulated debt. By the year 2021, over 105 years of gross savings will be required to repay accumulated debt.

Graph 5.1

Click on (Tables 26, 27 & 28) above

AMERICA IS OPERATING AT A LOSS

The aforementioned facts called for a deeper probe into the subject of profits, savings, and debt expansion. If profits are decreasing as a percentage of National Income, how can the economy create more jobs, more savings, and less debt? Obviously, more borrowing and more compound interest generates higher ratios of capital debt to profits and savings! This increased burden forces more unemployment on the economy!

The Board of Governors of the Federal Reserve produced data to support this logic. In 1990, 1991 & 1992, the creation of new private debt slowed. However, a dramatic expansion in public debt occurred. These developments are very similar to the events of the 1930, 1931 & 1932. Also, private debt expansion peaked at double digit levels in 1984-85-86, averaging over 13.5% of National Income for the 3 year period. This is similar to the debt expansion of the 1920's.

The Federal Reserve's data showed that the massive debt expansion of the 1980's had the temporary effect of reducing annual budget deficits. However, to reduce the deficit from 207.8 Billion Dollars in 1983 to 152.5 Billion Dollars in 1989, 3.7 Trillion Dollars of additional public and private debt was created.

This increase caused a consistent net operating loss or negative return on investment that averaged a minus 1.177% from 1983 through 1989 which in current dollars totaled 1,227.9 Trillion Dollars in total operating losses.

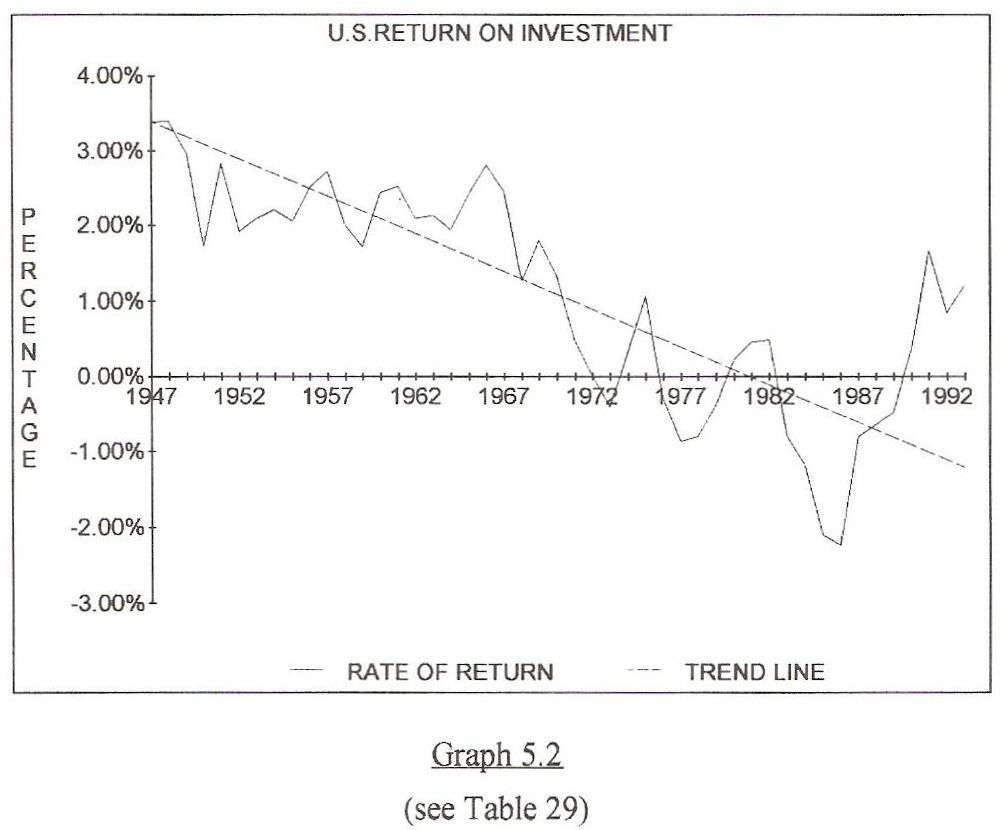

CALCULATING RETURN ON INVESTMENT

To calculate the nation's return on investment, first total the amount of money that accumulated annually in the "capital pool." This pool is the annual capital available for investment. The "capital pool" is the cash earnings accrued from corporate profits, net interest and rental income. Then, subtract annual public and private debt expansion from the "capital pool." The product, expressed as percentage of Domestic Wealth is America's return on investment.

When Americans borrow (either publicly or privately) more than the available capital, a net operating loss is produced. Debt can't grow faster than the capital pool which is the liquidity available for investment. However, that happened during most of the 1970's and the 1980's.

Graph 5.2

If total return on investment is viewed on a straight line computerized average, (a long term trend line) it's obvious that since 1970, return on investment has become a zero sum game. This indicates that Americans have borrowed too much to finance consumption while earning too little debt free money into circulation.

If debt grows faster that either National Income or Domestic Wealth, too much debt has been created. The economy is now torn between interest driven inflation and repeated periods of recession. Both are the result of too much annual debt expansion.

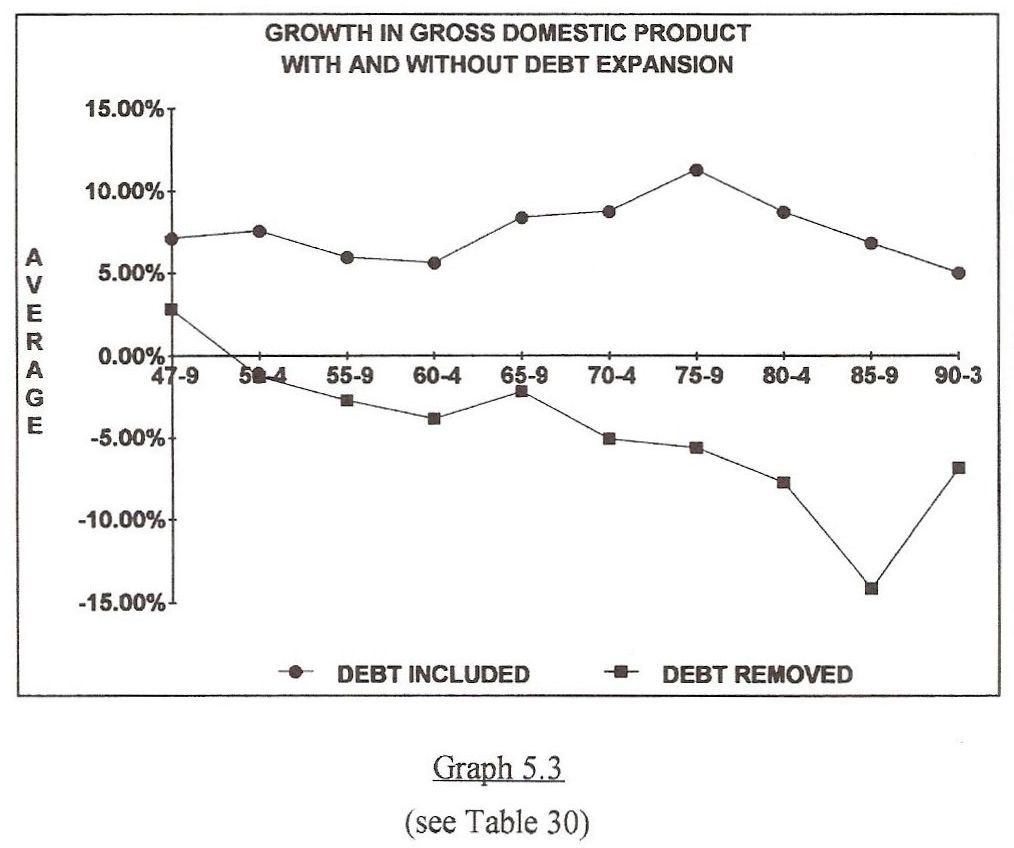

DEFINING GROWTH

What is growth? Is growth an increase to earned income, or an increase to debt? Or, is growth a combination of the two? The Commerce Department defines growth as the overall increase in GDP, net of inflation. In other words, if GDP increased by an annual rate of 6% and the rate of inflation was 3%, the Commerce Department reports a growth rate of 3% (6% nominal growth minus 3% inflation equals 3% reported growth).

In terms of Raw Materials Economics, no growth exists if growth is actually the growth of monetized debt which temporarily takes on the character of growth, but eventually becomes permanent debt expansion.

Graph 5.3

Graph 5.3 defines growth within the context of profit and loss. The graph reflects two series of five year average values. One is the perceived growth of GDP expressed in percentages. The other is net growth of GDP, after subtracting public and private debt expansion. Whenever gross debt expansion is subtracted from the annual change in GDP, a minus value appears.

This graph expands the logic behind a "base period" of 1947-49, which was the last time GDP experienced growth without the necessity for debt expansion.

Today, all growth in GDP is the growth of debt. Therefore, Americans owe for everything they accomplish.

THE PERFECT PARADOX

Here is a perfect paradox. Americans borrow for almost everything, but if borrowing stops or slows down as it did during 1990 & 1991, the economy collapses. Private debt expansion which was in a runaway during most of the 1980's, dropped to a post WWII low of 1.45% of National Income in 1991, and the economy soon stalled. So obviously, borrowing must continue as long as the economy remains out of balance.

However, more borrowing is damaging. In 1992 & 1993 more borrowing occurred and private debt expansion rose to a 24 month average of about 3.5% of National Income. The Federal Reserve reacted by raising interest rates 5 times during the first 7 months of 1994.

To summarize, excessive borrowing caused the economy to overheat and produce economic imbalances during the 1980's. Then borrowing was reduced, and this fueled the recession in 1991. So, borrowing had to be immediately resumed. When borrowing was resumed, the Federal Reserve restricted borrowing by raising interest rates.

So, there can be no cessation of borrowing, and there can be no increased level of borrowing without enlisting a negative reaction from the Federal Reserve Board. This flaw in the monetary system leaves 8-1/2 million people unemployed, and 39 million people (15% of the American population) in permanent poverty.

Today, America's primary economic generator, private debt expansion, is continuously restrained. However, the American public can't afford to restrain it, and the American public can't afford to borrow more!

Pastor Thomas Robert Malthus writing in "Essays On Population" said a person born into a world already full and in no need of additional labor was "redundant on the earth." This hard hearted conclusion is true today only because public policies are trapping future generations in poverty and debt.

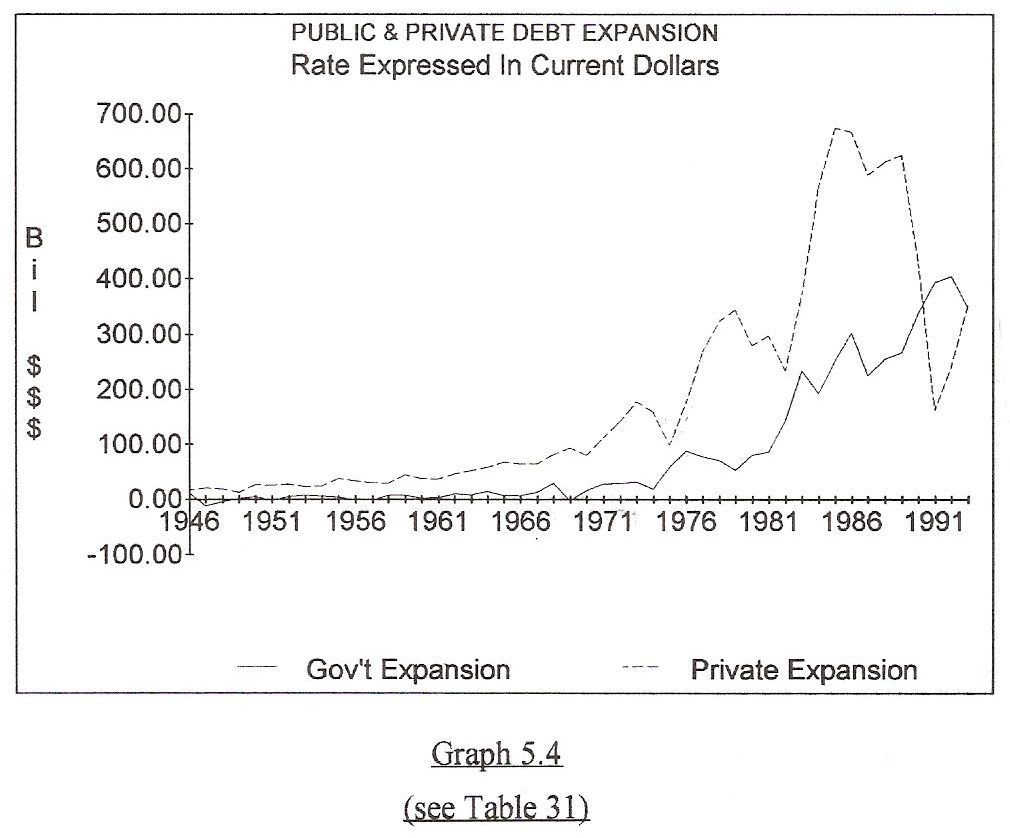

Graph 5.4

THE HISTORY OF PUBLIC & PRIVATE DEBT EXPANSION

A severe contraction of private debt occurred concurrently with an offsetting expansion of public debt in the 1930's. During that period, Americans eliminated private debt through deflation, bankruptcy and foreclosure, and debt reductions totaled 31.5 Billion Dollars from the period 1929 through 1941. During the same period, public debt expanded from 16.9 to 49.0 Billion Dollars, or a total of 32.1 Billion Dollars. This caused a net washout or (national economic) gain of zero after interest payments on public debt. During that period, National Income dropped from 85.3 Billion Dollars to 40.2 Billion Dollars and did not recover the 1929 level until December of 1940 when it reached 79.9 Billion Dollars. This is the sad legacy of New Deal programs that most Americans refuse to acknowledge. New Deal programs put food in stomachs and created non-wealth producing jobs, but a general restoration of balanced price levels were necessary before true recovery could occur.

A 19th century economist named Frederic Bastiat condemned public debt more than 150 years ago with these words: "Everyone wants to live at the expense of the state. They forget that the state lives at the expense of everyone." For that reason, deficit spending by government to assist a low profit economy is futile.

The New Deal of the 1930's was a failure! It cured nothing. It should illustrate that the solution to debt and unemployment cannot be more debt and under-employment.

Before the Great Depression, Americans were producing many forms of wealth such as grains and cattle, oil & gas, and mined minerals, etc. Millions were engaged in manufacturing trucks, cars, homes, office buildings, roads and bridges. However, after the stock market crash, too little currency and credit existed to distribute wealth because the currency and collateral value needed to generate distribution and consumption had been extinguished. To make matters worse, the Federal Reserve refused to pump replacement money into the economy. So, America had a surplus of goods in the middle of a hungry and unemployed country that couldn't exchange its labor for the goods and services of others. Instead of restoring the currency to a level that could properly represent the wealth in economic pipelines and warehouses, the government sponsored soup lines for the unemployed while it promoted the killing of livestock and their burial in ditches while a few months earlier, farmers had burned corn in wood heating stoves because there was no cash market for grain.

Instead of printing and circulating currency to reflect the nation's productive capacity so the economy could regenerate its previous patterns of production and consumption, the government allowed new private wealth and business activity to decrease until the remaining skeleton matched the existing level of currency and credit in circulation.

The following story as told by Charles E. Ball, was first printed in "The Finishing Touch," a history of the Texas Cattle Raisers Association and Cattle Feeding in the Southwest. It describes the hopelessness of the great depression. This story is entitled "The Day They Shot Our Cattle"

As a 10-year old boy on a small East Texas farm, it didn't take a lot to impress me. But one thing that really impressed me was the day they shot our cattle.

We had about 30 head, counting calves, which we fed and named and occasionally rode in a kids rodeo. In the summer of 1934, it was hot and dry: the sky was occasionally clouded with dust that blew in from West Texas; our pastures were extremely short; the cattle were unseasonably thin; the creek had dried up; and our three ponds were mere mud holes. We were hauling water from a neighbor's well - but the cattle just stood around the water trough, always thirsty. Obviously, they should be sold. Everybody wanted to sell. But there was absolutely no market. And many cattle were dying from starvation.

President Roosevelt's "New Deal" program, called the AAA, was offering relief to farmers who would plow up cotton (we did) or kill little pigs (we didn't), but independent, strong-willed cattle industry leaders were holding out. They had too much pride and self-determination to accept government help. But when you run out of water, pride and self-determination tend to wither, also. Finally, in June 1934, we heard on the radio that Congress had approved cattle as a basic commodity and appropriated $63 million for purchase and slaughter programs. Cattle in good shape would be purchased, slaughtered in local abattoirs, canned by people on work-relief and given to the poor. Cattle that were too thin (like ours) would be condemned and shot on the spot.

For several weeks, my dad and mom agonized over whether to have our cattle shot. Dad pointed out that the government was offering (for condemned cattle) $12 per head for those over 2 years of age, $10 for yearlings, and $4 for calves, "pretty good, considering these times." Furthermore, the price included a "benefit program" for producers with mortgaged cattle, which meant the banker wouldn't get more that half the payment. For cattle not condemned, the price was much better: $12 to $20 for those over 2 years, $10 to $15 for yearlings and $4 to $8 for calves.

As we waited, the cattle were getting poorer, we were pulling more of them out of the mud holes and hauling water was becoming "less noble." So my dad gave in.

Two government agents arrived late in the afternoon with high powered rifles; we had all our cattle penned in a lot right behind our house; and the big man simply said, "Which ones?" Dad would point to one - starting with the weakest and ugliest - and they would shoot. After about 12 deaths, it became harder and harder for my dad to point. In less than one hour, the men left, leaving 18 dead cattle in our lot. Neighbors came and took two of the fatter calves to dress that night. The next day, we drug the remaining dead cattle to the back of the pasture, where the buzzards and coyotes had a feast.

A lot of other cattlemen went through similar experiences. Within eight months, the government purchased 8.3 million head, reducing the U.S. cattle population by 11 percent. The average price paid was $13.50 per head. (editors note: $13.50 equals $109.91 in 1994 Dollars)

Since that period, the American economy has grown in size and maturity. The federal government has created social and financial safeguards to prevent this debauchery from repeating itself. As a result, America has permanent farm programs, Social Security, the Securities and Exchange Commission, Medicare & Medicaid, Workers Compensation and subsidies of various kinds, all designed to keep the economy alive past the time when the actual ratios and trend lines point to a depression.

Expenditures by federal agencies are safeguards that re-distribute wealth to compensate for internal economic imbalances. This has exchanged the economic cliff of the 1930's for the gentle slope of the 1990's. Redistribution won't restore an economy that's out of balance with itself. Redistribution adds nothing to the economy in terms of earned income or the profits of private enterprise.

During the 1920's, the general population had little understanding of wealth. They believed big Wall Street holding companies were capable of producing miracle profits while their underlying stocks paid no dividends.

Even though society was more sophisticated, the same thing occurred during the 1980's as millions of Americans were convinced that paper profits from Wall Street could create prosperity. At that time, all the trend lines proved America was past due for another depression, but it was postponed with false prosperity created by public and private debt expansion.

Noted economist John Kenneth Galbraith said it best in his 50th anniversary edition of The Crash of 1929:

Financial insanity can be a source of pure enjoyment. He added scornfully, Wall Street is like a lonely and accomplished woman who must wear black cotton stockings, heavy woolen underwear and parade her knowledge as a cook because unhappily, her supreme accomplishment is as a harlot.

If the value of raw materials, wages and consumer goods and services are in relative balance, a depression like the depression of the 1930's is impossible.

Under the Raw Materials Economics system, underlying values of stocks are determined by healthy dividends. This prevents a stock market crash.

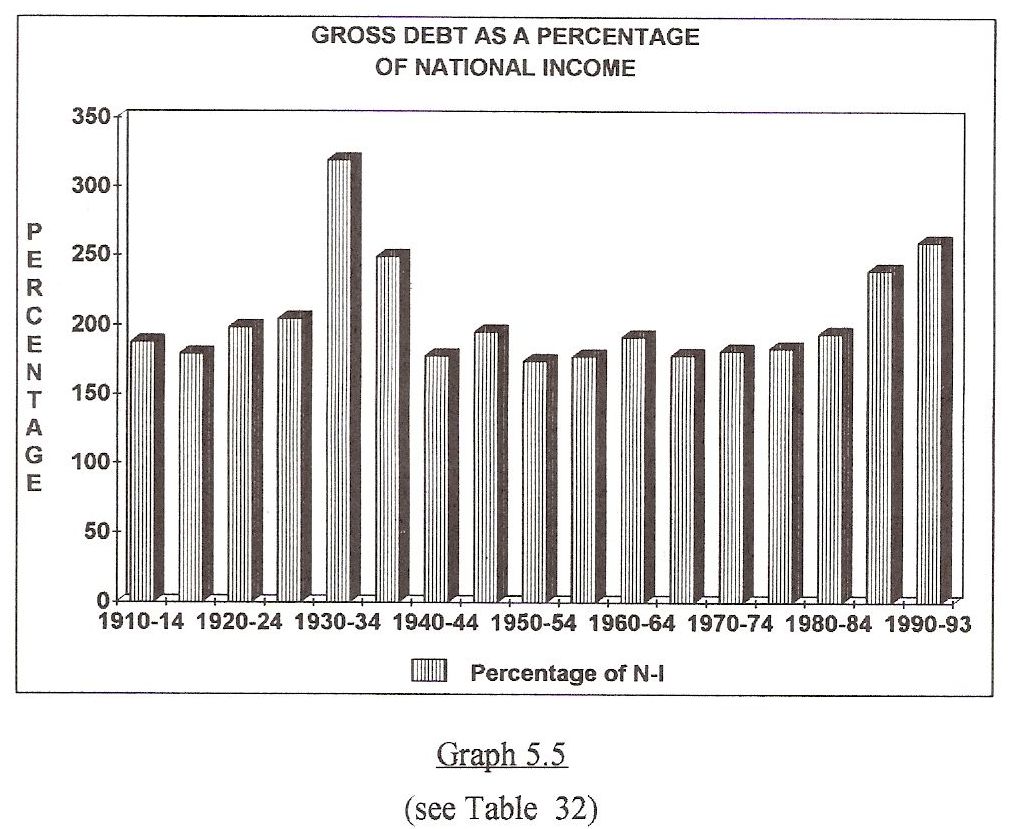

Graph 5.5

Graph 5.5 displays public and private debt as a percentage of annual National Income. This percentage has increased dramatically since the early 1980's. During the 1990-93 period, total debt averaged about 260% of National Income, and this percentage continues to grow. The economy hit rock bottom during 1930-34 period when 319% of one years National Income was necessary to repay debt. When viewed historically, we can conclude that debt as a percentage of National Income is reaching depression levels.

Graph 5.6

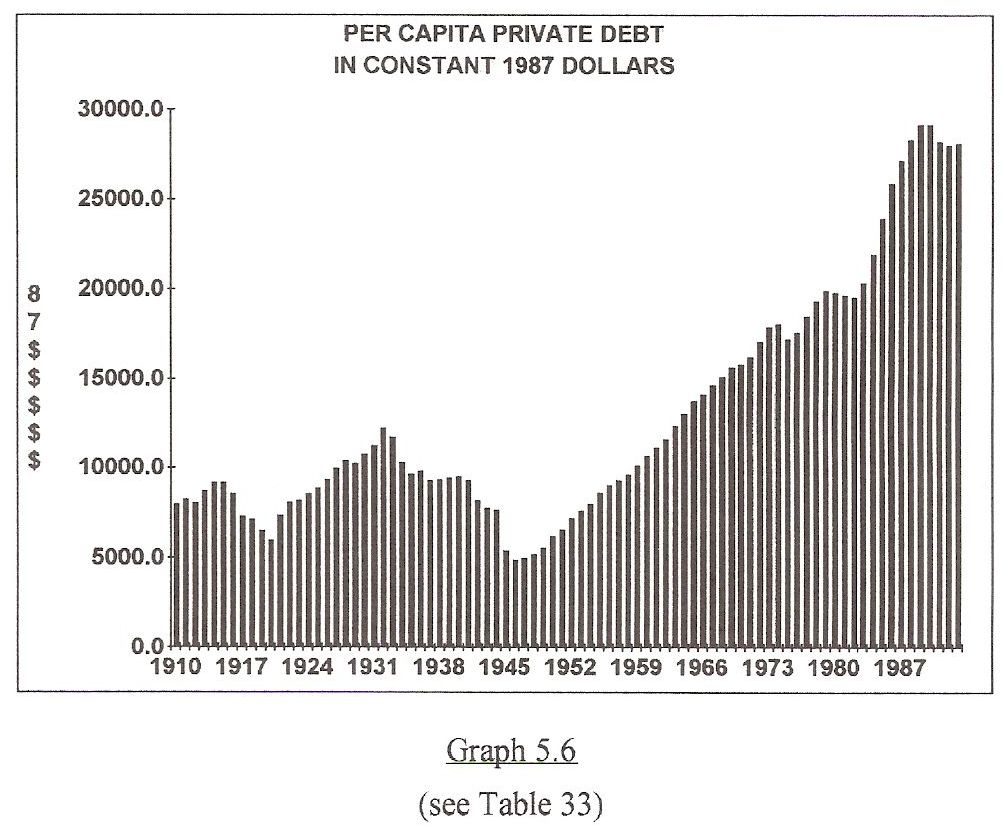

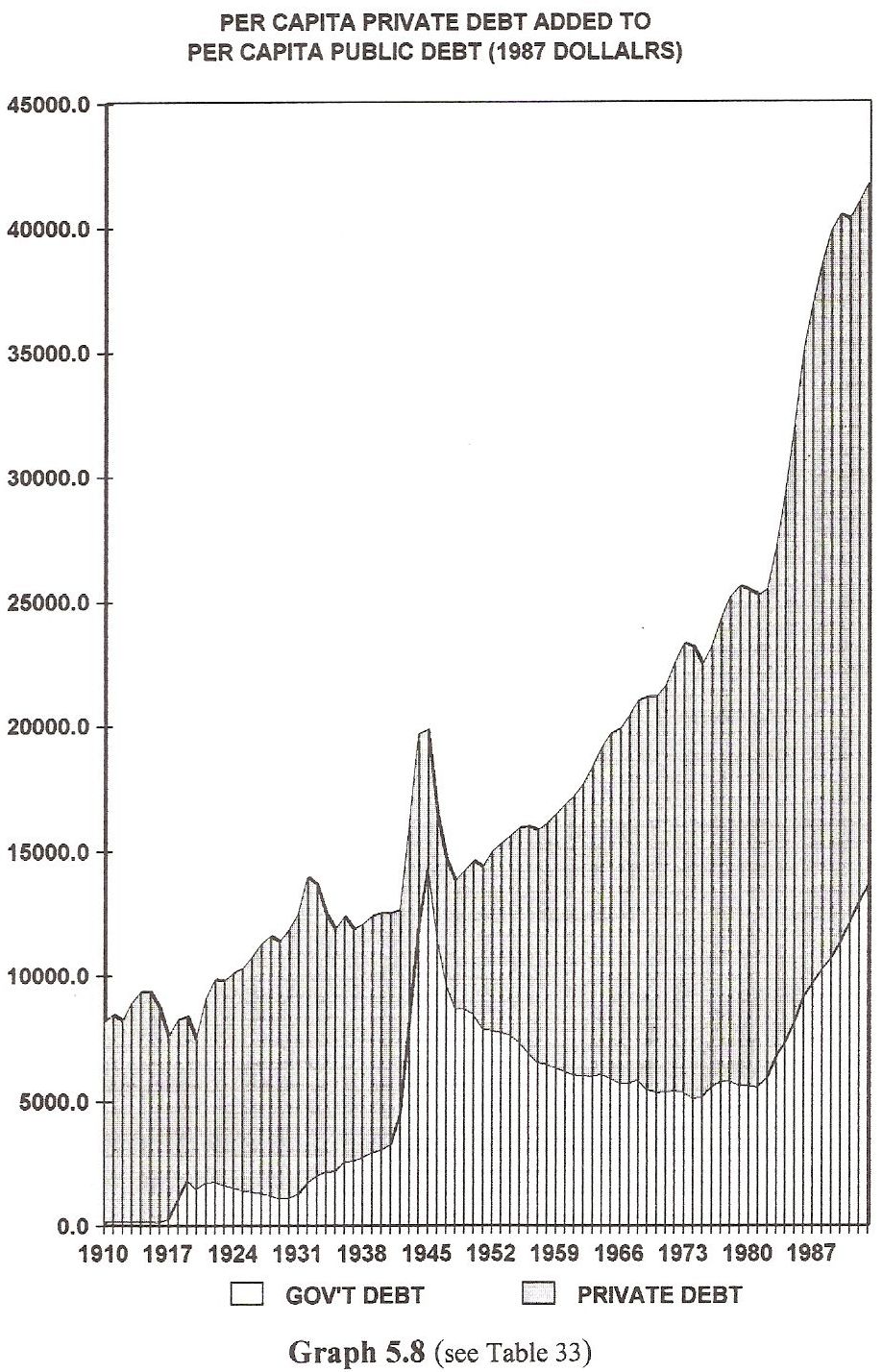

PER CAPITA PRIVATE DEBT

Graph 5.6 examines private debt on a per capita basis. It displays the average amount of private debt that each man, woman and child must pay. This examination has been conducted annually, and on 5 year averages on Table 33, so each year and each period can be summarized from 1910 through 1992.

The results are predictable. When raw materials sectors of the economy were in balance with processing, manufacturing and retailing, per capita private debt was low. In fact, per capita private debt reached an all time low of about $4500.00 measured in constant 1987 dollars during the 1946-50 period. During this period, production and consumption could occur without the necessity of creating capital debt.

Graph 5.7

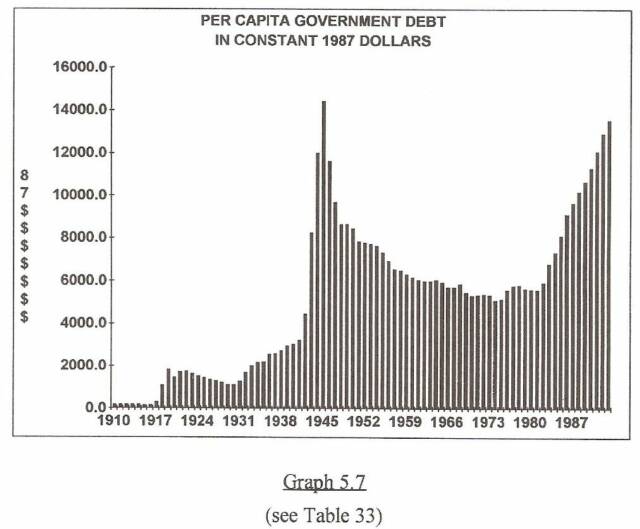

PER CAPITA PUBLIC DEBT

Per capita public debt reached an all time high of $11,775 at the end of WWII, just before the 1946-50 base period. But, since the prosperous private sector generated profits without the necessity of borrowing to consume, Americans repaid almost 1/2 of their total per capita debt in the 1946-50 "base period." As you can see, the debt line goes up dramatically during the early 40's and drops dramatically during the 1946-50 period.

At that time, many economists had forecast a recession or a depression similar to the depression of 1920-21 which followed WWI. The difference in price structure after these wars made the difference in postwar growth. At the end of WWI, prices were allowed to collapse, and the economy went into a tailspin. At the end of WWII, the economy continued to grow because retail prices were maintained in balance with the price of raw materials. Therefore, fundamental growth patterns were never interrupted. Instead, the economy was enhanced by a young and aggressive labor force that returned from the war.

These high levels of earned income carried over into the 1950's and continued to pay down the government's debt. However, the lower raw materials prices of the 1950's destroyed the balance between the beginning of the production cycle and the consuming end of the cycle so the economy had to generate offsetting levels of private debt for consumption to continue.

Total per capita public and private debt decreased slightly on two other occasions. Both decreases followed periods of higher raw materials prices.

From 1973 through 1975, per capita debt fell by $888 from $19,250 to $18,362. This occurred because money was earned into the economy at the beginning of the annual production cycle as a direct result of higher farm prices which peaked at 91% of USDA calculated parity. Also, during the oil boom, per capita public and private debt dropped from the 1979 level of $21,200 to $20,780 approximately 24 months later, a definite annual drop of $417 per person.

During the 1973-75 period and the 1978-81 period, America experienced recessions, which are temporary declines in GDP. These declines were not caused by the so called inflationary aspects of high commodity prices. Instead, these recessions were caused by the Federal Reserve's inappropriate reaction to higher raw materials prices.

Any time raw materials prices rise, the Federal Reserve increases interest rates, which interrupts the economy's attempt to re-establish balanced prices. This action slows monetary expansion and this interferes with consumption patterns. Thus, the Federal Reserve causes recessions by attempting to (tighten the money supply and) "hold down inflation." In effect, any time raw materials prices rise, the Federal Reserve creates a situation that lowers the commodity value of raw materials and raises the commodity value of money. This caused real value to be transferred from tangibles into debt instruments.

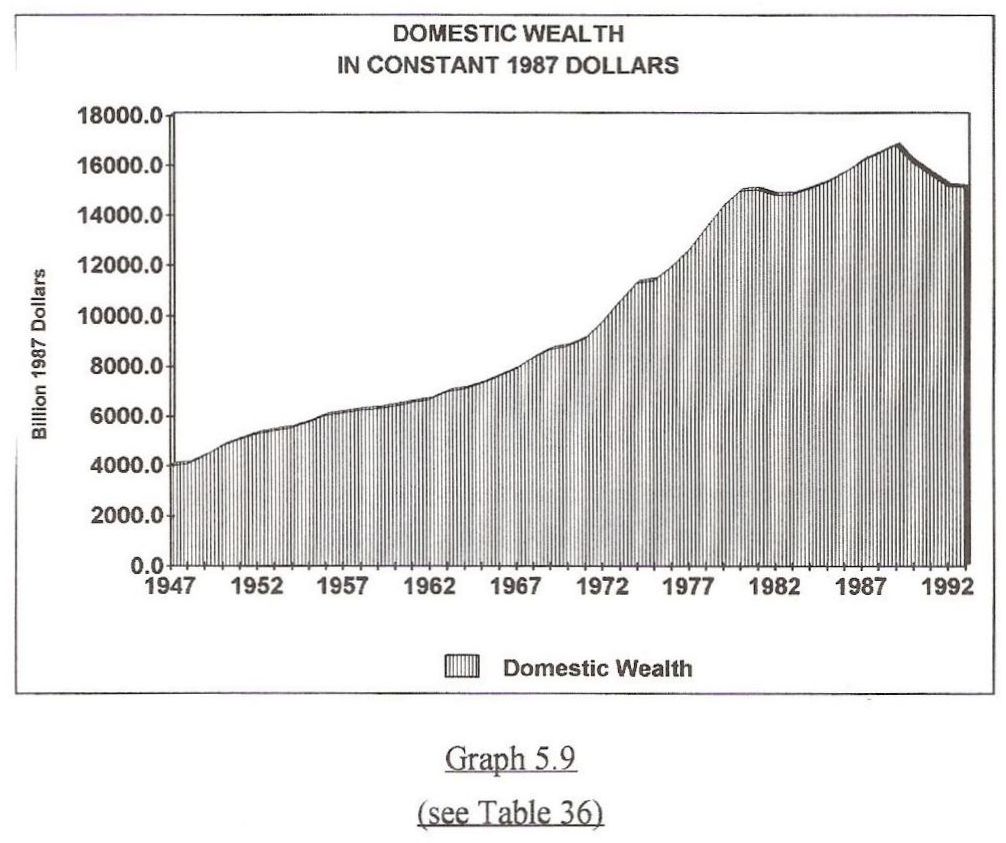

Graph 5.9

LOSS OF DOMESTIC WEALTH

Reflections upon these facts bring a host of new questions to the table. If individuals and companies of the 1990's borrowed all they could borrow, or refused to borrow (or banks wouldn't allow them to borrow) to re-invest, and if deficit spending by government which began in the 1930's and continued into the 1990's is no longer advantageous, then what remains? In other words, the classic Keynesian economic model of borrow and spend will no longer compensate for an imbalanced economy because the economy has gotten too far out of balance. What about the future? Can Americans maintain the ability to create Domestic Wealth when debt ratios are increasing?

Statistics from the Bureau of Economic Analysis (BEA) supplied answers. BEA statistics confirm that Domestic Wealth, which is roughly defined as the total replacement value of everything labor and technology has constructed from raw materials, has actually decreased after reaching a peak during the 1980's. When these facts are charted in constant dollars, (another way of saying "adjusting inflation out of the numbers") one learns that America has become poorer each year since 1989, and by 1993, domestic wealth had dropped to the same level as 1981. See Graph 5.9.

If gainful employment is to be found for the additional young people entering the work force each year and for more than 8-1/2 million now unemployed, Americans must either borrow or earn a lot of additional money into existence, or be satisfied with a stabilized recession that guarantees a generation of unemployed people.

What amount of money must be borrowed, invested, or earned into circulation each year to maintain prosperity? What volume of income is necessary to generate a level of National Income sufficient to support the new people entering the work force? Will more National Income re-establish 2 to 1 ratios of cost to profits on the T-charts?

A careful examination of the long term average ratios of profits to costs from 1929-1992, illustrate that historical trends are not sufficient to maintain the integrity of the private enterprise system. Americans have been earning too little and borrowing too much for a long time. This discovery was made by projecting the economy forward in time on a mathematical straight line using historical ratios of profits to cost as a baseline for predictions. The inputs for this exercise are the actual data stream of profits and costs since 1929 provided by the U.S. government.

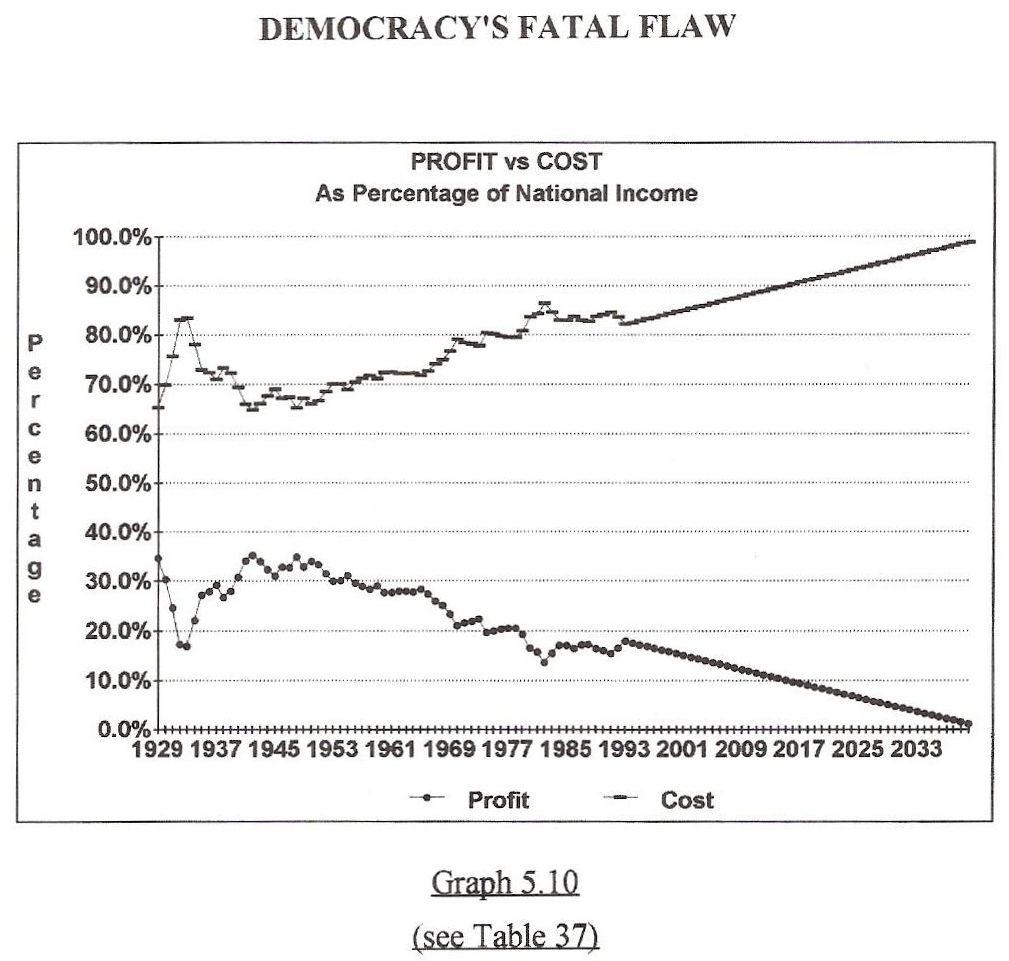

DEMOCRACY'S FATAL FLAW

Graph 5.10

NO PROFIT EQUALS NO PRIVATE ENTERPRISE SYSTEM

Graph 5.10 proves the long term trend lines of cost to profit established since 1929 will lead to the end of the American private enterprise system during the early part of the 21st century.

On this graph, the great depression is a prominent feature. It's defined by the first big upward spike in costs reflected on the upper line and also by the associated drop in profits reflected on the lower line. The period of profit stability after the depression is quite apparent, as is the declining profitability of recent years.

Graph 5.10 suggests the worst times are ahead. These projections indicate that before the year 2030, the private enterprise system, America's system of private, individual diversified ownership, will consolidate into a centralized system because without a sufficient profit, diversification of business ownership is impossible to maintain. How low a level of profit and how high a level of cost can the private enterprise system endure? The economy is in un-chartered but very instructive territory.

Graph 5.10 proves that if the American economy is to restore a sustainable level of profitability so its citizens can maintain the individual ownership of property and business, policy makers must do more than tweak the economy around the edges. Instead, law makers must stop the monetizing of debt and immediately construct national policies that restore the intrinsic values to production, labor, and property at all stages of the annual economic cycle. This graph leaves no question as to the cumulative effect of low profitability, and the effect of deteriorating skilled wages.

This graph reflects two opposing views of the world from two of the most quoted philosophers and economists of all time; John Maynard Keynes and Karl Marx! These men had an equal impact on the world but in vastly different ways. Keynes believed an economy could use government deficits as a springboard to prosperity. Keynes' belief was generally accepted until it took a brutal beating during the 1980's.

Marx represented the other end of the spectrum. He believed a capitalist system would fail because private businesses destroy their profitability through destructive competition. If Marx had been alive during the 1930's, he would have surely declared capitalism dead, as did Stalin and other communist leaders of the day. Strangely enough, it was Keynesian economics that kept the American system alive during the great depression. In fact, Keynesian economics fueled the American economy until federal laws were enacted in the 1940's that restored the value of many basic items of tangible production.

Graph 5.10 expresses America's economic history as defined by the ideas, knowledge, visions, and mistakes of both men. Marx was wrong when he said a capitalist system is doomed to fail, and Keynes was wrong for believing that a capitalist system can be sustained with debt. Neither man understood the physical economy. This missing link prevented them from making a mathematical circle around their theories. So they stood, 359 degrees apart, face to face, separated by a very narrow and deep abyss.

Today, America is on a trend line that ends in the dismantling of private enterprise around the year 2030. Coincidentally, this is the year Keynes said would usher in a utopian period of wealth and prosperity. According to Keynes, the year 2030 will begin a period when all wants and needs will be satisfied. Look at Graph 5.10 and draw your own conclusions!

It's a summary of America's monetary and fiscal policies. It proves the additional borrowing necessary to generate growth will be impossible to repay when combined with total annual accumulated interest.

Graph 5.10 proves the current situation of falling profitability only gets worse with more borrowing, causing total economic costs to finally consume total economic profits. Thus, more borrowing eventually becomes impossible without hyper-inflation.

The records prove the manipulation of interest rates and creative attempts to borrow and spend the country out of debt are futile.

Every American should be very concerned by the quality of leadership demonstrated by those who believe the economy is on course.

Table 37 is the mathematical counterpart to Graph 5.10. It describes the actual condition of all segments of National Income and projects them forward assuming no meaningful corrections occur. As you can see, the economy completely loses its structure around the year 2020.

A STUDY OF BASE PERIODS

Thus far, we've proven that average long term trends of costs to profits from 1929 through 1993 are inadequate to restore the natural price equilibrium to our nation's economy. So, shorter periods of time must be examined; times when debts were low and the country was prosperous. These shorter periods generally occur in 3 to 5 or even 10 year spans. They can be used as a blueprint for prosperity.

During these "base periods," costs became balanced with profits at a ratio of about 2 parts cost to 1 part profit (before taxes), that when combined, comprised the balanced contributing factors to National Income. Table 39, indicates that such a base period occurred shortly after WWII. This period will be established as a standard for calculating adequate future levels of National Income.

This base period, which existed from 1946 through 1950 yielded prosperity to all five segments of the nation's economy. At that time, the country was experiencing an explosion of prosperity. In fact, wage and price controls had to be maintained after WWII to insure that the economy wouldn't overheat. This occurred in a post war period that many economists had wrongly declared would be deflationary. This post war period of prosperity might seem to be an anomaly that might never repeat itself. In fact, it was the inevitable result of maintaining the par exchange value between raw materials and finished goods which enabled earned income to roll through the economy, generating employment and prosperity.

By correctly analyzing this base period, we can create a hypothetical economy that might have existed if base period percentages of profitability and cost had continued to the present day.

Table 38 projects this balanced base period into the year 2020. In this hypothetical economy, the 8.7% of National Income now consumed by Net Interest was reduced to the base period level of under 1-1/2%, and that level was maintained until the year 2020. Net farm income was lowered from 7.6% of National Income during the base period to about 3% by the year 2020. Since agriculture leads the way toward a more sophisticated society by producing more food with a smaller percentage of the population, its percentage must be decreased slightly. This change releases a larger percentage of new workers into the production of high tech items. This allows the remaining components of National Income to grow and add to technology, but the real growth began with reciprocal increases to efficiency that flowed between agriculture and other components of private enterprise. This reciprocal flow of efficiency improves the well being of all sectors of the economy.

Since high tech items must be produced at a profit and purchased with earned income, these projections move net business income from 10.4% of National Income in the base period to 12.1% by 2020. Also, corporate profits move from 11.7% of National Income during the base period to 14.8% by the year 2020, and rental incomes move from 2.9% of National Income to 3.4%.

The profits of private enterprise should always total approximately 1/3 of National Income for any year of the projection, just as they did during the base period. This is true even during the year 2020.

Table 40 demonstrates a pattern for a balanced economy. This Table does not reflect the actual situation. Instead, it's the situation that would have existed if America had maintained the standard of the base period.

For this table, a shorter base period of, 1947-49 is used. This base period was used by the U.S. government during the decade of the 1950's. However, several other periods yield similar results. As already described, the five year base period of 1946 through 1950 is appropriate as is the period of 1947-49. Also, the years 1948-50 can be used. These base periods yield the same results as a longer period that began in 1943 and ended in 1952. These base periods are equally suitable, not because of war, not because of inflation, not because of exploding productivity, but because raw materials prices were kept in balance with wages, interest, and consumer goods.

Table 40 leaves the question outstanding. Are these economic solutions possible?

A BALANCED NATIONAL INCOME

The structurally balanced economy depicted in Table 38 required several continuing adjustments to the percentage of National Income attributable to each segment of the economy. A growing economy is fluid, not static, and when it's operated at naturally balanced prices, it continuously creates improved efficiency which produces small and predictable changes in the percentages of National Income attributable to the economic segments displayed on the profit side, or the left side of the T-chart. These numbers and percentages confirm that agriculture must lead the way to a high tech, well fed, and prosperous economy.

Various model adjustments automatically occur in a balanced (or par) economy that acknowledge steady technological advances. These advances require specific amounts of income in specific segments of the economy.

As technology advances, the percentage of National Income earned by all raw materials producers, those engaged in crop and livestock farming, oil & gas production, mining, forestry, commercial fishing and recycling are naturally reduced. This makes room for the development, production, distribution and sale of more high tech items.

This should not cause these basic industries to suffer a deterioration of profits as has been the situation in America. Overall profitability should never deteriorate due to efficiency. Instead, a constant, measurable. and predictable movement of new labor into high tech manufacturing and selected essential services will occur as technology advances society toward more efficient levels of raw materials production and use. These are appropriate changes in the division of labor that should never decrease profitability. These changes should always result in a consistent percentage of National Income for the left side of the T-chart (the profits of private enterprise). These advances in technology should lead to natural increases to efficiency and should not throw farmers off the land or send wildcatters to other continents. Instead, a normal re-dividing of the labor force should occur as efficiency slowly releases a larger percentage of new workers to non basic industries. If the economy remains in balance during this process, the money (barter power) will automatically exist to sustain prosperity. Students of Raw Materials Economics refer to this natural progression as an expanding trade turn and labor turn. The concept of this natural progression will be studied in future chapters.

It might appear that optimal ratios of income to cost are restored by returning each segment of the economy to the percentage of National Income earned during the most recent base period of high profitability, 1947-48-49. However, a rigid restoration of base period percentages of income to cost for each individual profit producing segment of the economy will result in a giant step backward for society because improvements to technology allow more jobs to be created outside basic industries and more labor to be performed by new people entering the work force that produce and distribute new high tech items. These workers act in reciprocal harmony with each other to improve the efficiency of the economy. Since people follow money, and money is the paper reflection of wealth, then the money to pay for new technology must be present in each sector of the economy. Otherwise, the people will follow the money back to the land, or congregate in ghettos.

If technology had not advanced since the base period, the number of persons engaged in raw materials production today would be doubled from the 1947-49 base period level in order to supply the growing population. In other words, without a constant increase in efficiency, the economy would demand that 21 million people be engaged in farming, mining, fishing, logging and recycling. If America had a balanced economy and full employment today, only 11 to 12 million people would be on the land, not 21 million.

In 1994, the American economy employed only 4 million people in raw materials production, and 8.5 million people were unemployed. That reflects an economy out of balance with itself. Again, technology changes the division of labor by assisting people in basic industries and manufacturing. This assistance allows basic industries to produce more of natures materials for an expanding population. Today, Americans live under public policies that push the economy too fast. This forces structural unemployment and poverty on a growing percentage of the population.

THE PRODUCTION OF EFFICIENT HORSEPOWER

More efficient horsepower is the single best example of how technology pulls efficiency forward. One "horsepower" is the energy required to lift 550 pounds, a distance of one foot, in one second. More efficient horsepower is a technological advancement that alters the division of labor. When America farmed with horses and mules, a farmer needed to grow a certain amount of grain to feed draft animals. Today, farmers either plant and sell their grain for cash, or in the form of animal meat. The cash earned from these sales is used to pay production expenses that include the cost of mechanical horsepower and the cost of electricity, diesel fuel, natural gas, propane, or gasoline. So the acreage formerly used to feed draft animals now produces cash crops that pay for the refined fuel and more "efficient horsepower."

THE EFFICIENCY OF LABOR

Labor increases its efficiency by aiding in the consolidation and sophistication of its duties. This improves the product of its efforts. In the past, farm workers were assigned the job of hand weeding (hoeing). Today, synthetic chemical compounds and more sophisticated management procedures have replaced much of this labor.

Hand picking or pulling of cotton is another excellent example. Before mechanical cotton harvesters were invented, a strong man could pick 300 pounds of seed cotton per day. This same man could pull 500 pounds of cotton bolies, burrs and all, per day. The hardest worker, calculated separately, could harvest a single bale of cotton in 4 to 5 days. Today, with mechanical harvesters, one person can harvest several bales of cotton per hour.

This harvesting speed suggests that clothes should be very cheap. This is not true because the labor cost of harvesting didn't disappear. Instead, the labor simply moved to a city and was paid to build a more efficient mechanical harvester. Today's cotton farmer pays most of the harvesting cost to a manufacturer who employs hundreds of urban workers to build harvesting machines. A net efficiency gain occurs through this process which reduces the farm portion of proprietors income from about 8.7% of National Income during the base period years of 1947-48-49, to about 3% of National Income by the year 2020.

The formula used to determine this natural change involves the calculation of a slowly moving ratio. The methodology to analyze this ratio was used during the 1930,s by an industrial engineer named Charles Ray, one of the founders of the Raw Materials National Council. As you will see in upcoming chapters, the concept behind this moving ratio is quite simple and is based upon the changes of prices and production output from a base period standard of 100. Ray used this concept to correctly forecast the economy while under contract to Sears, Roebuck & Co.

The Charles Ray formula which proposes a reduction in agriculture's percentage of National Income from 8.7% in 1950 to about 3% of National Income by the year 2020, allocates a proper share of National Income to off-farm technological advances. It does not translate into public policies that blindly remove people from the basic industries of agriculture, fishing, forestry, mining, etc. To the contrary, Too many people have already been forced away from these occupations, and into cities where they compete with a surplus urban workforce for jobs! THIS IS THE SOURCE OF AMERICA'S STRUCTURAL UNEMPLOYMENT!

In fact, this wholesale evacuation of income and people from rural America has removed 5 million full time farmers from the land since 1950. When all basic industries are considered, the number increases to 8.5 million, a number that approximates total unemployment today!. Again, in a structurally balanced economy, about 12 million people would be farming, fishing, logging, mining etc. In other words, the base period ratio of raw materials workers to the total industrial workforce was about 1 to 5 during 1947-49. In 1994 it should have increased to about 1 to 7.3. This is the true measure of improved efficiency. Instead, we have less than 4 million people employed in raw materials production. The remainder have re-surfaced as the surplus urban work force that must be supported by welfare or some other type of transfer payments.

This is the consequence of stripping the economic base away from millions of citizens. Downsizing America's basic industries has reduced farm income from a 1950 level of over 7% of National Income, to less than 1 percent of National Income today. Also, low oil prices has caused America to import over 1/2 of its oil. Artificially low oil prices encourage over-consumption and discourage the development of sustainable energy sources. In the long run, the dismantling of these basic new wealth industries has permanently displaced of over 8.5 million workers. These workers were dislocated by a structural (economic) imbalance within the American economy. This explanation should give full meaning to the term "structural unemployment."

If the America economy had remained in structural balance since the last base period, a larger percentage of the new work force would continuously be channeled to high tech jobs as the economy expanded over time. As a result of these modifications to the division of labor, the gross raw materials income at the first point of sale, earned by agriculture, forestry, commercial fishing, mining, and recycling would gradually decrease as a percentage of National Income. This natural decrease only stops when society stops making net improvements to efficiency.

The economy is now operating as though raw material producers were as efficient as the food replicators and dilithium energy crystals depicted on the Star Trek television series. As ridiculous as it sounds, that's exactly how National Income is apportioned. This ms-apportionment of income increases debt and forces too many raw materials producers out of business and forces the remaining producers to cut costs to a non-sustaining level. These surviving producers are less likely to expend the money and effort necessary to be good stewards of the land, water and air.

National policies must maintain a correct percentage of income and population within basic industries, or much of the labor force assigned to basic industries and the employees of companies that supply retail inputs to these industries will produce unemployment. This has occurred in America.

A pre-mature attempt to re-assign the labor force to high tech jobs and non-essential services has failed to stabilize prosperity. Instead, it has created a syndrome of income destruction. This syndrome began in crude oil production and then moved into agriculture. The syndrome forces imported oil on the population; it evacuates the countryside of farmers, and it retards the development of alternative energy sources.

Generally speaking, public policy has pushed efficiency so hard that it causes labor exploitation and the abuse of the planet's natural resource base. It has also eliminated millions of skilled jobs in America. This has destroyed the reciprocal harmony of increased efficiency. This internal reciprocity must be restored so America can grow and prosper.

When essential domestic industries are downsized, money is borrowed to purchase the same products from other nations. This expands public debt and does nothing to support the displaced work force. This has occurred in petroleum, agriculture, forestry and fishery industries, and this impacts manufacturing, distribution and consumption. It causes poverty, under-employment and unemployment.

Since the gross income of basic industries (agriculture, forestry, fishing, mining etc.) is produced at the beginning of each production cycle, the gross income paid to these industries automatically limits the prices they pay for retail production inputs. In turn, this income (the income paid for production inputs at retail by raw materials producers) establishes a foundation under the price of skilled labor. These skilled laborers are the same laborers that purchase the most expensive consumer goods and put the greatest strain on the economy when they are unemployed.

THE ECONOMY HAS A NATURAL ORDER

The economy is a naturally integrated system with a point of beginning and a point of conclusion for each product or service. The economy's natural economic cycle begins with the purchase of inputs needed by raw materials producers and the cycle is complete when the consumption of consumer goods and services occur. This is called a production cycle. It is the necessary production of product and income created by the harmonious reciprocal markets of citizens who produce, distribute and consume goods and services. Therefore, it becomes necessary to quantify the amount of gross income that must be earned by all producers at the first point of sale in order to maintain price levels without the artificial supplement of debt expansion. This necessary price level flows from the beginning of the production cycle as retail inputs are purchased by raw materials producers. This is the systemic price creating mechanism in a "for profit" economy. This natural system establishes the price floor under essential goods and services.

When prices for raw materials are maintained at parity, they become a structural guarantee against depressions or currency debasement for the entire national economy. This price level at the first point of sale ultimately determines if a country creates wealth or debt during each production cycle. Therefore, the level at which a country prices its raw materials will ultimately determine that country's standard of living.

It should be mentioned that island nations with shortages of natural resources can establish a par economy by importing cheap raw materials and then raising the price of those materials to their full domestic parity value before they enter domestic channels of commerce. Thus, the difference between the cost of their raw material imports and their higher domestic price level creates a rollover of income and produces a macro economic effect similar to domestically produced raw materials.

Under current trade practices, nations that import raw materials must find trading partners (such as the United States) who are willing to sell raw materials at below parity while importing manufactured goods at full parity and endure the trade deficits these exchanges produce. If each nation exported and imported products and services at their domestic par value, this form of trade exploitation could not exist because tariffs and duties would consistently maintain trade reciprocity. This natural order is another cornerstone of Raw Materials Economics.